Greece Faces Energy Shock Risks from Middle East War, but Eurozone Is a Shield

The Greek economy is showing strong fiscal performance, resilient growth and significant progress in the labour market, yet it continues to face structural challenges and new external risks. In this environment, the war in the Middle East is creating another energy shock for the global economy, with potential implications for inflation and businesses, according to remarks made during a Fitch Ratings webinar on Greece attended by Naftemporiki.gr.

Responding to a question from Naftemporiki about the impact of the Middle East conflict, Greg Kiss stressed that the war represents another shock for the global economy, primarily through energy markets. He estimated, however, that the conflict could last less than a month and highlighted the “shield” Greece enjoys.

“The war in the Middle East is a new shock for the global economy. We have already seen significant damage to energy facilities across the Gulf,” he said. According to him, the main impact will come from the energy supply side, which could lead to higher prices and renewed inflationary pressures worldwide. “The shock to energy supply will lead to higher inflation and intensify pressure on the global economy,” he noted.

Despite the concerns, Fitch believes the impact could remain limited if the crisis does not drag on.

“We believe the conflict could last less than a month,” Greg Kiss said, adding that under such a scenario Greece’s growth rate could remain close to 2%.

The Eurozone “shield” for Greece

Regarding Greece, Greg Kiss stressed that the country’s participation in the Eurozone is an important factor of stability during periods of international turbulence.

“It is important to say that Greece benefits from being a member of the Eurozone. This is a very important shield for the country,” he said.

At the same time, he noted that Greece continues to enjoy particularly favourable financing conditions, which makes it less vulnerable to the impact of tighter monetary policy compared with other economies.

However, there is also a clear point of vulnerability: the country’s dependence on energy imports.

“The main vulnerability of Greece relates to its reliance on energy imports,” he said, stressing that a prolonged energy shock could affect the economy mainly through higher prices.

The labour market has changed dramatically since the crisis

One of the most encouraging developments for the Greek economy is the significant improvement in the labour market.

As Greg Kiss noted, employment has returned to the levels seen in 2010, although today’s economic landscape is very different from the pre-crisis period.

“Employment has returned to the levels of 2010, but the Greek economy of 2026 is very different and the population has declined,” he said.

Today, the 4.5 million people employed represent a higher employment rate than before the crisis.

At the same time, he warned that the overall picture should not be viewed as overly optimistic, as persistent structural weaknesses linked to the crisis years remain.

“I don’t want to give an overly optimistic picture because there are legacy issues,” he said.

The legacy of the crisis and the per capita income gap

According to Fitch, one of the key challenges for the Greek economy remains the level of per capita income.

As Greg Kiss noted, Greece’s GDP per capita relative to the European average continues to represent a significant challenge, particularly when compared with the progress made by countries in Central and Eastern Europe after joining the European Union.

This gap is largely a legacy of the sovereign debt crisis, which sharply reduced Greek incomes and the country’s overall economic output.

Despite the improvements of recent years, this lag indicates that the Greek economy still has some way to go before fully converging with the European average.

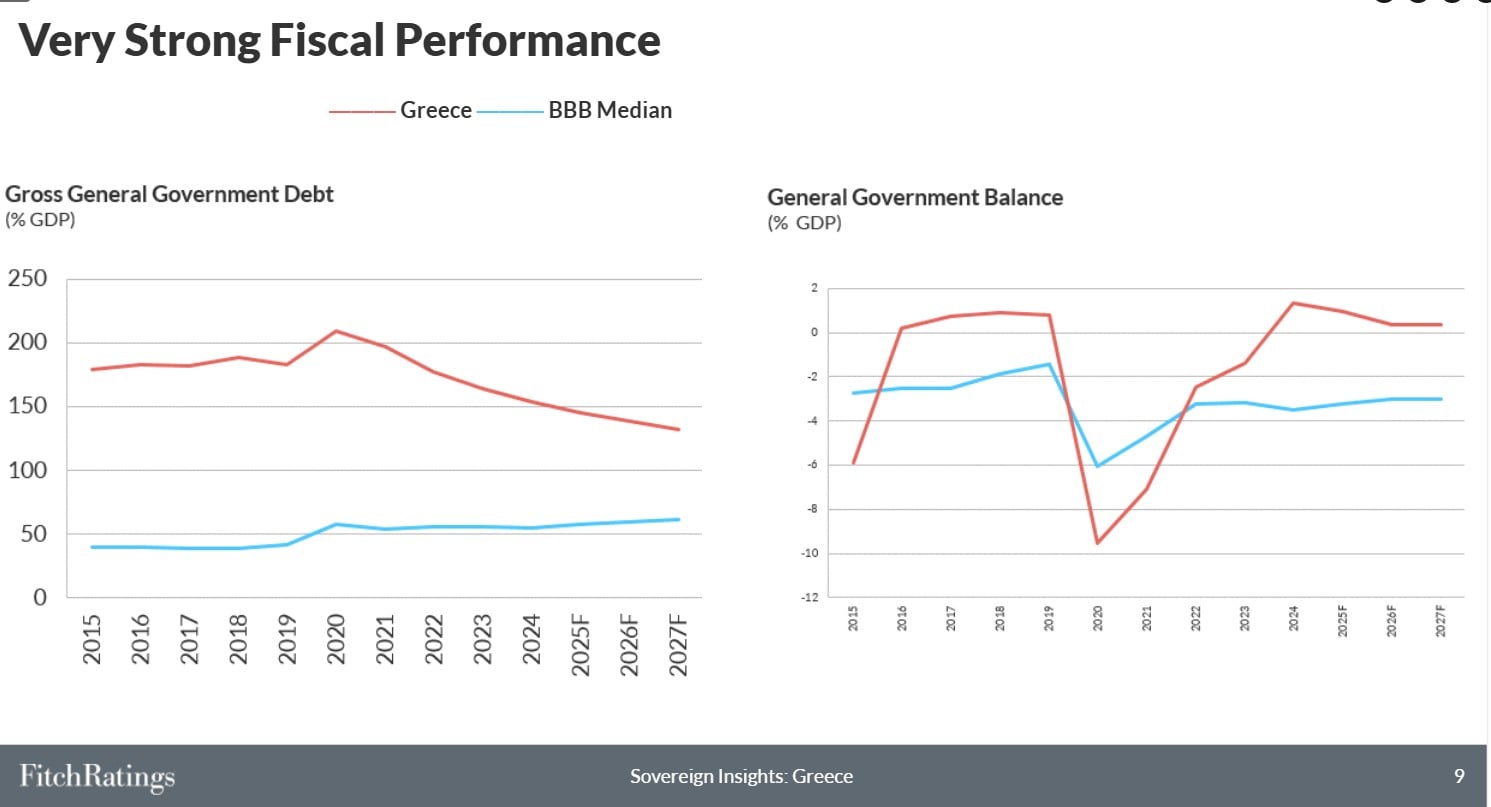

Very strong fiscal performance

Fitch places particular emphasis on the country’s public finances, which it describes as particularly strong.

Greece is running primary budget surpluses — something that, as Kiss noted, is relatively rare not only in the Eurozone but also globally.

Fiscal performance has also been supported by significant structural changes. One factor highlighted by the agency is the reduction of public consumption as a share of GDP, which is seen as an indication that fiscal adjustment has become more structural.

At the same time, Greece benefits from favourable financing conditions.

As Kiss explained, the country continues to benefit from the favourable loan terms associated with past financial support programmes. Even if Greece were to rely entirely on market financing, borrowing conditions would remain favourable.

Another important factor, according to Fitch, is the broad political consensus around fiscal discipline, which strengthens the credibility of economic policy.

Debt expected to decline further

Fitch expects Greece’s public debt to continue declining over the coming years.

According to the agency’s projections, public debt, which stood at 164% of GDP in 2023, is expected to fall:

- to 145% in 2025,

- to 138% in 2026,

- and to 132% in 2027.

This trajectory reflects the combination of strong primary surpluses and positive economic growth.

Tax cuts and support measures without fiscal strain

Within the fiscal policy framework, Fitch notes that certain measures supporting the economy — such as tax cuts and housing rent subsidies — have been designed in a way that does not create significant fiscal pressure.

According to Greg Kiss, these measures have a positive fiscal multiplier, meaning they support economic activity without materially burdening public finances.

Greece’s rating and outlook

Fitch also recalled that it upgraded Greece in November, reflecting the improvement in the country’s economic fundamentals.

Greece is now rated BBB, within the investment-grade category. As Greg Kiss noted, this rating is mainly based on the country’s strong fiscal position, the steady decline in public debt and the resilience of the economy.

Within Fitch’s rating scale, Greece stands slightly below countries such as Italy and Bulgaria, which are rated BBB+.

Banks: strong profitability and loan growth

The presentation also examined the performance of the banking sector, which has improved significantly in recent years.

Greek banks are showing:

- loan growth of about 8% in 2025,

- a strong increase in fee income,

- and solid operating profitability.

Fitch expects National Bank of Greece and Eurobank to have positive rating outlooks, while a potential upgrade for Alpha Bank and Piraeus Bank would require further improvements in asset quality.

Despite the progress, the sovereign–bank link remains, mainly through deferred tax credits of around €12 billion and public guarantees of about €18 billion related to securitisation schemes for non-performing loans.

External risks and the Iran war

Speaking about the broader global environment, Emmanuel Bulle, Senior Director and Head of Research for corporates in EMEA and APAC at Fitch Ratings, warned that the conflict involving Iran could prove prolonged and have significant implications for businesses.

“If history is any guide, this type of conflict can last quite a while and could have a significant impact on corporates,” he said.

According to Bulle, a prolonged geopolitical crisis could affect multiple areas of the global economy, including:

- energy prices

- inflation

- bond spreads

- global supply chains.

“There are many risks,” he stressed, adding that Fitch is still assessing the overall impact.

Some sectors could benefit, however. Utilities, for example, could see improved revenues due to higher natural gas prices. By contrast, sectors such as tourism and transportation could face pressure if the crisis persists.